The Markets

September strikes again…

If you look back over the last 20 years, September has been the worst performing month for the Standard & Poor’s 500 Index, according to Nasdaq.

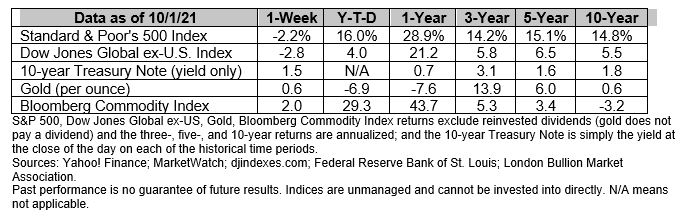

This year, the S&P 500 dropped 4.8 percent in September. That wasn’t enough to wipe out gains from earlier in the third quarter, and the Index finished the quarter slightly higher. The Dow Jones Industrial Average and the Nasdaq Composite Index also tumbled in September. Their losses erased the previous two month’s gains, so the Dow and Nasdaq finished the quarter lower than they started it, reported Caitlin McCabe and Caitlin Ostroff of The Wall Street Journal.

Investors had a lot to consider during September and over the third quarter, including:

- Resurgence of the coronavirus. On July 1, the seven-day moving average of coronavirus cases in the United States was about 14,500. Early September, the average had rocketed to about 170,000. By the end of September, the average was trending lower, reported the Centers for Disease Control.

One result of COVID-19 is that life expectancy at birth fell from 2019 to 2020. In the United States, life expectancy at birth has fallen by more than one year. Italy, Poland and Spain also have seen life expectancy drop by more than one year, reported The Economist. Lifespan increased in two countries: Denmark and Norway.

- Global economic growth concerns. The resurgence of COVID-19 also dented global business executives’ confidence that the world economy will improve during the next six months, according to latest McKinsey Global Survey. While the majority (71 percent) of those surveyed said that economic conditions will improve in the coming months, the number was lower than the prior quarter’s 81 percent. Survey respondents said the top risks to economic growth were the pandemic, supply chain disruptions and inflation.

- Supply chain disruptions. The supply chains issues created by the pandemic have not been easy to resolve. David Lynch of The Washington Post reported:

“The commercial pipeline that each year brings $1 trillion worth of toys, clothing, electronics and furniture from Asia to the United States is clogged and no one knows how to unclog it…the median cost of shipping a standard rectangular metal container from China to the West Coast of the United States hit a record $20,586, almost twice what it cost in July, which was twice what it cost in January, according to the Freightos index. Essential freight-handling equipment too often is not where it’s needed, and when it is, there aren’t enough truckers or warehouse workers to operate it.” Toward the end of September, more than 70 container ships were anchored near the West coast, waiting for a berth to open so goods could be delivered.

- Rising inflation. The cost of producing goods has been increasing. “The producer price index, a proxy for corporate or wholesaler costs, has risen for eight months in a row and, in August, was up 10.5% from a year earlier, the highest reading since June 1981. Compare this to the consumer price index, a proxy for realized manufacturer or retailer prices, which was up 5.3%. This 5.2-percentage-point gap is one of the largest in more than 40 years, suggesting higher costs are outpacing merchant end-prices…,” reported Lisa Shalett of Morgan Stanley. When producer costs rise faster than consumer prices, companies’ profitability may drop and that could negatively affect earnings.

- Tightening central bank policy. The Federal Reserve is concerned about inflation, too, and is considering a move toward less accommodative monetary policy. In late September, Federal officials indicated that tapering – slowly reducing monthly purchases of securities – could begin later this year. Once purchases have ended, the Fed could begin to raise interest rates in late 2022 or 2023, depending on how the economy is growing, reported Jonnelle Marte of Reuters.

As if these issues weren’t enough, investors also had to process the potential effects of a global energy crisis, China’s regulatory crackdown, and another U.S. debt-ceiling standoff.

Despite these challenges, the fourth quarter got off to a good start on Friday. Eighty percent of the companies in the S&P 500 saw their share prices rise. The S&P 500 gained 1.2 percent for the day, while the Dow rose 1.4 percent, and the Nasdaq gained 0.8 percent, reported Jacob Sonenshine and Jack Denton of Barron’s.