After the market closed on Wednesday, April 2, the President announced new “reciprocal” tariffs on nearly every nation.

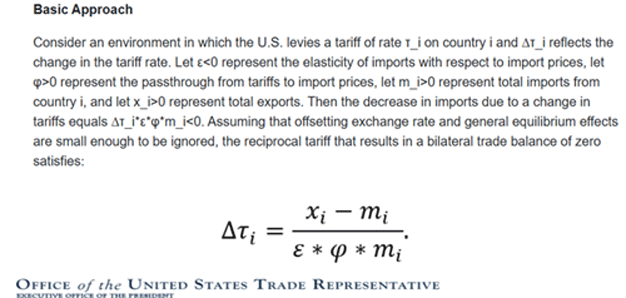

How were tariffs calculated?

Figure 1: The Tariff Formula

In plain language, let’s use China as an example (WSJ).

Divide the U.S. 2024 goods-trade deficit of $295 billion by the amount the U.S. imported from China—$439 billion. That equals 67%. Apply a 50% discount, and China’s reciprocal tariff equals 34%.

This is the tariff formula.

Due to tit-for-tat retaliation, 34% has increased to 125%, plus an additional 20% for the “fentanyl penalty.” At that rate, most trade is likely to freeze up.

A minimum of 10% on goods was levied on nearly all nations.

Reaction

Economic visibility is extremely limited today. Given already high valuations, “Liberation Day” levies lopped 10.5% off the S&P 500 Index in just two days. Carnage in stocks spread to the Treasury market as longer-term yields, which initially fell in a safe-haven play, surged.

Moreover, weakness in Treasuries, coupled with a drop in the dollar, raised fears that a full-blown crisis might erupt, which led the President to implement a 90-day pause on reciprocal levies. Sector-specific and baseline tariffs remain in place.

The tariff situation is evolving, and Trump exempted various electronics, including iPhones, from reciprocal tariffs over the weekend. He warned that these exemptions might not last.

While much of the economic data suggests that the U.S. economy continues to expand, soft surveys such as consumer and business confidence have sagged, leading to fears that U.S. economic growth will slow or, worse, slip into a recession.

Earlier this month, the government reported a stronger-than-expected increase in nonfarm payrolls of 228,000 in March. Last week, the core CPI unexpectedly slowed to 0.06%.

Absent the drama from tariffs, I suspect investor chatter surrounding the potential for nearer-term rate cuts and a soft landing would be driving stocks to new highs. But that is not the reality of today’s environment.

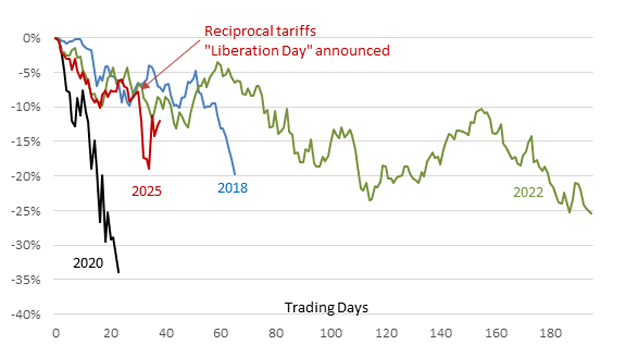

1. Comparative damage

- How does the market carnage stack up with the Covid bear market and recent corrections (2023’s 10% pullback excluded)?

- Through April 14, the S&P 500 has retraced about one-third of its decline.

Figure 2: S&P 500 Pullbacks, Peak to Trough

Data Source: St. Louis Federal Reserve 4/14/2025

Returns do not include reinvested dividends.

Past performance is no guarantee of future results.

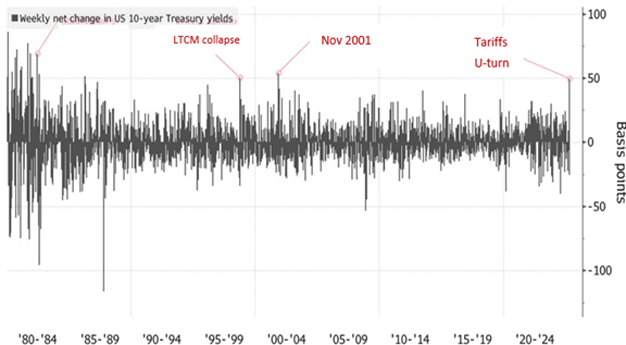

2. Tariffs, Treasuries, the deficit, the dollar

- Heightened market uncertainty usually leads to increased interest in Treasuries. Put simply, sell the riskier assets (like stocks) and stash the cash into ultra-safe Treasuries.

- Additionally, overseas buyers seek safety in U.S. dollars, which would typically find their way into Treasuries.

- That paradigm broke down last week.

- The 10-year Treasury yield bottomed on Friday, April 4, at 3.86% in intra-day trading.

- The benchmark bond yield peaked at nearly 4.60% one week later.

- Net change for the week: +47 basis points.

- The Bloomberg U.S. Agg Total Return fell 2.5% over the five-day period.

Figure 3: Tariff Yield Action Rivals Historic Meltdowns

Source: Bloomberg

- The ICE BofAML MOVE Index, which reflects volatility in U.S. Treasury futures (think of it as a VIX Index for bonds), hit its highest level since the financial crisis.

- The Dollar Index is at a three-year low.

- The implementation of reciprocal tariffs not only generated a tsunami that walloped stocks, but the impact rocked the bedrock of the global financial system: risk-free Treasuries (credit risk, not rate risk).

- The S&P 500 dropped 10.5% in two days—consider it a mini-crash, loosely defining a crash as a one-day 10% decline.

- Initially, the sharp market decline forced a reversal of leveraged trades.

- A quick way to raise cash—sell Treasury bonds, especially if margined.

- Sky-high reciprocal tariffs also ignited inflation worries, which may be discouraging some investors to seek safety in Treasury bonds.

- Fed Chief Powell is retreating from his baseline assumption at the March Fed meeting that any rise in tariff inflation would likely be temporary (he used the previously jettisoned “transitory” last month).

- Currently, weak growth and recession fears are overshadowed by the risk of higher inflation, influencing yields.

- A 0.06% rise in the core CPI in March did little to boost investor optimism on the rate-cut front.

- If economic weakness ensues, rising layoffs and weak job growth (or job losses), would likely prompt the Fed to act.

- Talk of sales by China and Japanese banks may be exacerbating worries.

- “The issue facing the markets is a loss of confidence in U.S. policy,” said Kathy Jones, chief fixed-income strategist at Charles Schwab.

- We are re-defining the risk-free rate of the world,” said Bhanu Baweja, chief strategist at UBS. “If you put volatility in the risk-free rate of the world, it will upend every market.”

- German bonds may be one recipient of liquidated Treasuries as the 10-year bund yield has fallen from 2.64% on Liberation Day to 2.51% as of April 14.

- Gold is up from $3,166 to $3,213 or 1.5%, while the S&P 500 is down 5.1% over the same period.

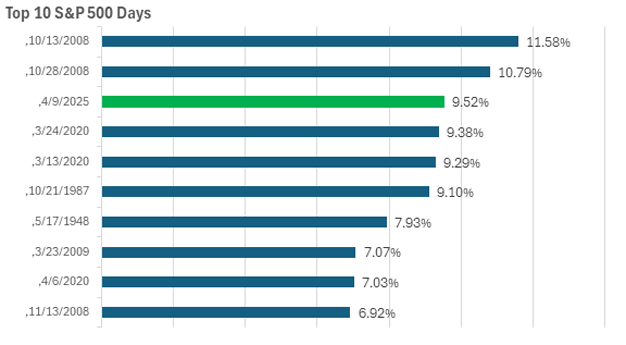

A 90-day delay

- Trump’s 90-day delay in reciprocal tariffs fueled the 3rd-biggest rise in the S&P 500 since WWII.

- On Thursday, he didn’t rule out another extension.

Figure 4: Liberation Day Delay Leads to Massive One-Day Gain

Data Source; FactSet, CNBC

The S&P 90 is used as a proxy prior to the creation of the S&P 500 Index in 1957.

- But tariffs remain a headwind.

- There is a baseline 10% tariff on goods, while imported steel, aluminum and autos (except USMCA-compliant autos) are taxed at 25%, per Reuters.

- Late last week, the average tariff rate was calculated at 18% ex-China. It rises to 25% when China’s 145% is included (125% reciprocal, 20% fentanyl-inspired tariff).

- 18% is far above the pre-Trump rate of about 3%.

- On Monday, Trump exempted electronics from China’s reciprocal rate.

- Unlike 1930’s Smoot-Hawley Tariff Act, most countries have held back on retaliation, at least so far.

- For now, an unwinnable “all-out” trade war has been averted.

Why did Trump shift gears?

- Tremors in the Treasury market

- An 18.9% decline in the S&P 500 from the February peak

- Lobbying by business leaders:

- Jamie Dimon: a recession is a “likely outcome”

- Bill Ackman’s X tweet: “We are heading for a self-induced, economic nuclear winter, and we should start hunkering down.”

A wrench in the economic gears

- Reciprocal tariffs got everyone’s attention—investors and CEOs.

- A survey of 329 CEOs and business owners (April 8–10) revealed that 76% believe it will hurt their business and 62% expect a slowdown or recession over the next six months.

- When confidence falls, businesses cut back capital expenditure plans, further exacerbating a tenuous economic situation.

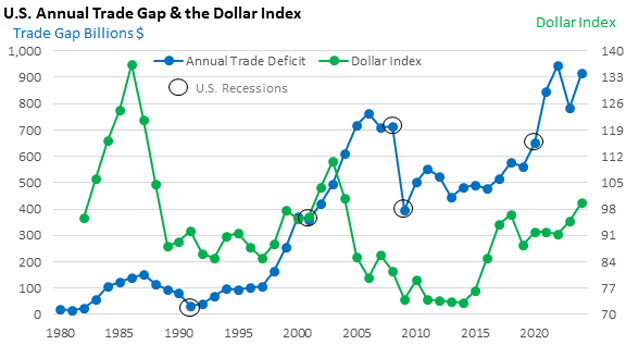

3. The dollar and the trade deficit

- The conventional wisdom suggests that the strength or weakness of the dollar plays a key role in a rising or falling trade deficit.

- A strong dollar makes imports cheaper and exports more expensive—the deficit should rise.

- A weak dollar makes imports more expensive and exports cheaper—the deficit should fall.

- Figure 5 illustrates the annual U.S. trade deficit (left axis) and compares it to the annual change in the Dollar Index (right axis).

- There is a two-year lag in the dollar.

Figure 5: The Dollar and the Deficit

Data Source: St. Louis Federal Reserve, 2024

- Put the brakes on conventional wisdom.

- The correlation between the two variables is -0.29, i.e., a rising dollar correlates to a minor decline in the deficit—counterintuitive.

- The deficit as a percent of GDP is nearly 0.

- Elasticity of demand may play a larger role.

- Example: a 10% rise in import prices would only decrease the value of imports if demand fell by more than 10%.

- Imports would be expected to rise as the U.S. economy expands.

- The U.S. is the wealthiest nation in the world. It is consumer-driven.

- Other factors: The 1990–91, 2001, and 2008–09 recessions temporarily lowered the trade gap, especially consumer spending in 2009.

- Rising U.S. oil output, which lessened oil imports, played a modest role in limiting the U.S. gap in the 2010s.

- A strong U.S. recovery from the Covid recession raised U.S. consumer spending; some of that spending found its way into imported goods.

- A cursory review of the data suggests the dollar does not have as big an impact as conventional wisdom would suggest.

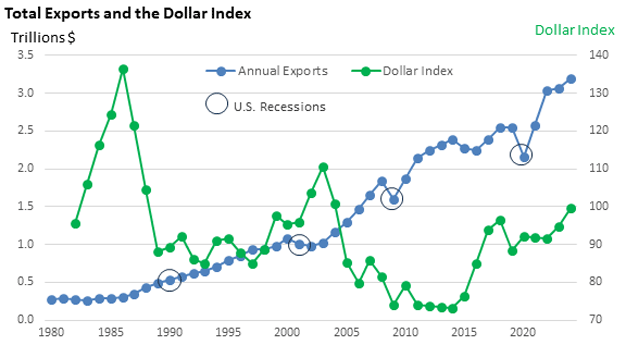

- Does a weaker dollar, which lowers export prices, aid exports?

Figure 6: One More Look

- There is an inverse correlation between the dollar and exports: -0.47, which would be expected.

- Other factors: An expanding global economy would also aid exports.

- Summary: It’s too simplistic to say the dollar is the key variable for imports and exports.

Dollar drivers

- Factors that drive the dollar include U.S. interest rates versus foreign rates, expectations of changes in interest rates, economic growth, and the overall stability of the U.S. as a safe place to invest.

- During the financial crisis, the dollar appreciated by 25%, despite the fact the crisis originated in the U.S. (subprime loans).

- During the Covid recession, the dollar rose by nearly 10%.

- During times of heightened uncertainty, the dollar historically comes out on top, as overseas funds seek safety, that is, until U.S. tariffs rocked global markets, and the dollar image was tarnished.

- Today, there isn’t an alternative to the dollar.

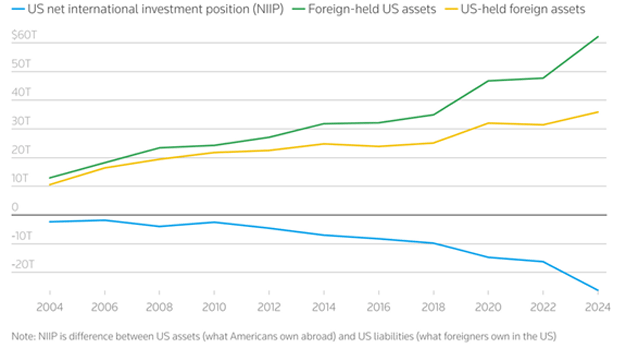

- Figure 7 highlights the uptrend in the dollar since 2014 and favorable capital inflows.

Figure 7: The U.S. is the Place to BeForeign holdings of U.S. assets surge to $62 trillion, driving dollar higher

Source: U.S. BEA, Reuters

- Past support for the dollar includes:

- U.S. exceptionalism,

- higher interest rates,

- strong portfolio inflows,

- and the overall stability of the U.S. economy, including strong institutions, a stable democracy, rule of law, and deep and transparent capital markets.

- Investors fear a U.S. policy shift and an upending of the global order, which was established by the U.S. after WWII, is underway, with no real alternative.

- April 2’s announcement had unintended consequences.

- A year from now, could this be a distant memory? It’s still too early to assess the long-term impact on Treasuries and the dollar.

- Deutsche Bank warned of a dollar crisis.

- Piper Sandler says it is still confident in the currency.

- In the near term, there’s significant pessimism; stocks often ascend amid concerns, yet the impact of tariffs on the economy remains uncertain.

Maybe, if the White House is able to conclude “one big, beautiful” trade bill.